Quick Answer

No-fault Accidents

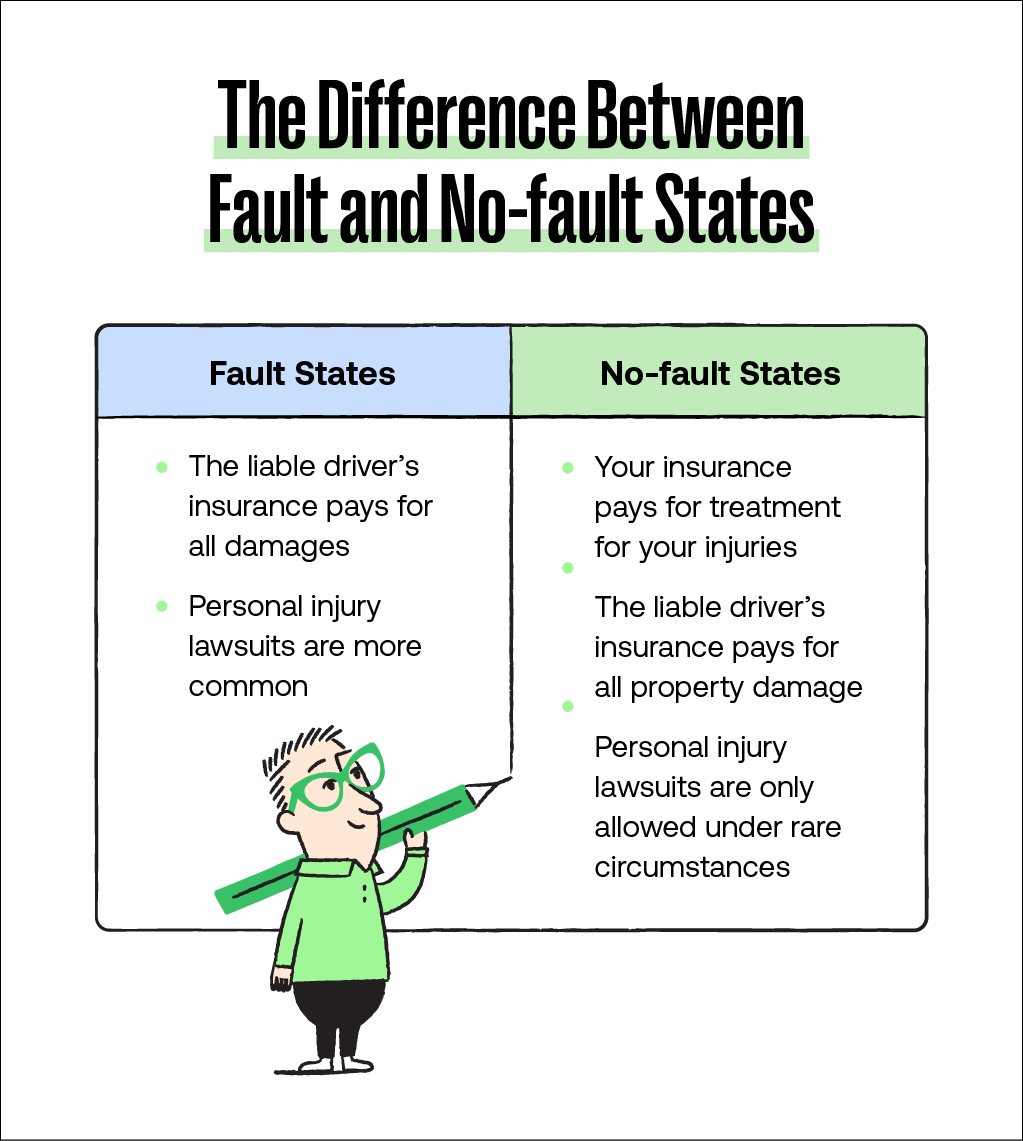

No-fault, also known as personal injury protection, is a type of coverage on your auto insurance policy which is required in some states to cover economic damages related to an injury. Each driver uses their required personal injury protection coverage to pay for their medical bills and lost wages. The driver who is responsible for the accident uses their insurance for any automotive damage and the innocent driver can pursue pain and suffering through the at fault driver’s insurance.

Assigning blame is the name of the game after a car crash.

After a car accident in a no-fault state, most people think their only options are figuring it out alone or immediately calling a lawyer. There's a smarter approach: Mighty can help you organize documentation, retrieve police reports and medical records, and understand what PIP covers and how claims are evaluated, helping you prepare your case without surrendering 33% to attorney fees.

If you live in a no-fault state or were involved in an accident in one, it's important to understand how the system works and how this third option fits into it. This guide breaks down how no-fault insurance affects liability, your rights, and the best path to recovering compensation.

But First, What Is No-fault Insurance (aka Personal Injury Protection Insurance)?

No-fault insurance means that in the event of a car accident, each driver is responsible for paying their own medical bill through their insurance. This requires an extra layer of protection known as personal injury protection (PIP), making insurance more expensive than in at-fault states.

For example, the state of New York requires registered motor vehicles to have liability insurance with certain minimum coverage amounts:

● $25,000/$50,000 for bodily injury per person

● $50,000/$100,000 for death

● $10,000 for property damage per accident

States use no-fault insurance in an attempt to keep personal injury lawsuits from clogging up the courts. If all drivers are required to have PIP, then they are less likely to seek damages from the other party.

This is where Mighty can help. Many people in no-fault states don't need a lawyer but still need help understanding what PIP covers, what documents their insurer expects, and how to avoid weakening their claim. Mighty can assist with organizing your documentation, retrieving police reports and medical records, and helping you understand the claims process without the 33% legal fees.

The process for claiming damages in a no-fault state is similar to at-fault states, only you won't be dealing with the other driver's insurance:

1) You'll notify your insurance that you were injured in an accident.

2) Their insurance adjuster will speak with you regarding your claim.

3) You'll provide them with your relevant medical records.

4) You'll submit all expenses related to your injury.

5) You'll negotiate with your insurance company for payment for medical bills and lost wage reimbursement.

If you aren't sure what to submit or how to structure your documentation, Mighty can help by retrieving your medical records, helping organize your expenses, and ensuring you understand what documents insurers typically expect.

Personal injury protection insurance generally excludes damages related to pain and suffering, so you won't be including things like emotional distress or inconvenience in your claim.

Our Opinion

"Personal injury law firms generally only help recover money for bodily injury and unfortunately that does not include the body of your car. The reason boils down to a personal injury lawyer's incentive: the money they make.

Traditional PI lawyers are not incentivized to help you repair your car. This is because the settlement you get at the end of your case, which your attorney gets his fee on, does not include damages to your car." — Mighty's take

What are No Fault Benefits?

No-fault benefits include medical bills, prescriptions, lost wages, housekeeping, and transportation paid regardless of who caused the accident.

Because these benefits have strict documentation and deadlines (like the 30-day PIP application window), it's important to stay organized and keep track of all deadlines. Mighty can help you understand these timelines and organize your documentation to ensure nothing gets missed, something that often hurts claim value.

And an Overview of Fault vs. No-fault States

States that assign fault to one party for medical costs are known as tort states. They work by making the at-fault driver responsible for paying both medical and vehicle repair costs for the injured party. They use bodily injury liability insurance and property damage liability insurance in lieu of PIP.

What are the states with no-fault insurance?

The following are states with No-fault insurance:

- Floria

- Hawaii

- Kansas

- Kentucky

- Massachusetts

- Michigan

- Minnnesota

- New Jersey

- New York

- North Dakota

- Pennsylvania

- Utah

Out of the above, three states allow drivers not to buy a no-fault car insurance policy, also known as "choice no-fault" states:

- Kentucky

- New Jersey

- Pennsylvania

So, Who Pays for Car Damage in a No-fault State?

Since no-fault insurance only applies to bodily injuries, the driver who is at fault for the accident is still responsible for the damage to the other driver’s property.

Personal injury protection insurance applies to:

- Medical bills

- Out-of-pocket expenses

- Lost wages

- Funeral expenses

- Essential services, like child care and yard work

This is an area where people often struggle on their own navigating what falls under PIP vs. property damage. Mighty can help break this down and assist with organizing documentation, helping you understand which documents typically go to which insurer for straightforward scenarios.

So, how do you go about getting your car repaired in a no-fault state? Here are your options.

Read More: Should I Get a Lawyer For An Accident That Wasn't My Fault

Scenario 1: You Use Your Collision Coverage or Comprehensive Coverage

Depending on how the car was damaged, you can make a claim to your insurance provider through your collision or comprehensive policy.

- Collision coverage pays for damage to your vehicle that was caused by another vehicle or object. Hitting a wall or guardrail would be considered a collision.

- Comprehensive coverage pays for damage to your vehicle not stemming from a collision. Theft and vandalization fall under comprehensive policies.

Speaking with your insurance company can clear up any confusion surrounding which policy applies to your specific car accident.

This coverage is optional and not cheap, so you’ll need to decide in advance whether or not the added protection is worth it.

Mighty can help you understand which coverage typically applies and assist with retrieving necessary documentation from repair shops, helping you organize your claim materials for submission to insurers.

Scenario 2: You Use the At-fault Driver’s Auto Insurance Policy

If the other driver is determined to be at fault for the accident, you can use their insurance policy to pay for your car repairs.

Their insurance provider will want to be sure their driver was at fault, so they’ll investigate your claim. You can help your case by having a police report that backs up your story and by documenting the scene of the accident with pictures or video.

If it’s unclear who is at fault for the accident, you can expect the insurance company to put up a fight.

Mighty can help by retrieving your police report and assisting with organizing all evidence (photos, witness statements, repair estimates) so you have everything documented and ready when the insurer evaluates your claim. This is the advantage of using Mighty: you're not alone in organizing your case, but you're also not giving up 33% of your recovery for assistance you can get with the right support.

Scenario 3: A Lawsuit Determines Who Pays

In the event of a coverage or liability dispute, you may need to resort to filing a lawsuit.

This is more complicated than going through insurance, so it’s recommended to bring in a qualified lawyer to assist you through the process.

For everything leading up to that point organizing documents, retrieving police reports and medical records, and understanding which policies apply Mighty can assist you. If the claim crosses into true litigation territory, that's when transitioning to an attorney makes sense.

Even in no-fault states, drivers who cause an accident can still be responsible for some personal injuries. If your injuries are eligible, you’ll need to claim them in the lawsuit from the very beginning. This is where a lawyer can step in and ensure you don’t accidentally waive your right to expensive damages.

Before escalating to a lawsuit, Mighty can help you organize your documentation and understand what records you have, making it easier to evaluate whether you need an attorney and ensuring any lawyer you do hire has everything properly organized from the start

Our Opinion

“...insurance companies often prolong the legal process, waging a war of attrition to get plaintiffs to accept quick, less-than-fair settlements. This happens even in the most clear-cut cases. It's called "frivolous defense," a phrase you will have heard much less frequently than "frivolous lawsuits," even though many scholars believe it is the former that causes our courts to clog, not the latter." — Mighty's take

And How Does Negligence Impact Liability?

Negligence is the deciding factor in determining liability for a car accident, and this even applies to a degree for a no-fault accident. If it’s not immediately clear who caused the accident, the insurance companies will use the evidence surrounding the case to piece together a narrative.

Negligence can be applied in several ways and can have a major impact on your claim:

- Pure contributory negligence: You’ll be barred from recovering damages if you contributed to the accident in any way.

- Pure comparative negligence: You can recover damages if the other party was even 1% at fault for the accident. Your recovery is reduced by your percentage of negligence.

- 50/50 comparative negligence: You can recover damages if you’re 50% or less at fault, but the amount you can recover is reduced by your percentage of liability.

- 51/49 comparative negligence: You must be less than 50% at fault to recover damages and the award is reduced by your liability.

How negligence is applied to your claim will depend on the laws in your state.

Many drivers struggle to understand how negligence rules impact their claim value or ability to recover damages. Understanding which negligence standard applies in your state and how insurers use it when evaluating your case can make it easier to present your claim clearly and avoid mistakes that reduce your payout.

Suing Another Driver

Yes, you can sue in a no-fault state, but it needs to meet certain standards. Just because no-fault insurance is in place to reduce personal injury lawsuits doesn’t mean they’re ruled out entirely. There are certain situations where you can recoup losses by suing the other driver.

No-fault insurance places a cap on how much it is able to cover. If your lost wages or medical expenses exceed the amount your PIP insurance covers, you can sue the other driver for the difference. You can also sue if the severity of your injuries exceed the state’s injury threshold.

In a similar vein, if the car accident has diminished your earning potential or will likely lead to future expenses, you can hold the other driver responsible.

Before escalating to a lawsuit, Mighty can help you organize your documentation and retrieve necessary records, making it easier to understand whether you actually meet the lawsuit threshold and what documentation you still need. This helps you make informed decisions about whether to hire an attorney and ensures you only pay for legal services when it truly adds value.

Suing Third Parties

In some cases, accidents can involve more than just you and the other driver. If a third party played a role in the accident, then they can and should be held responsible.

Third-party involvement can include:

- An auto shop failing to properly repair a vehicle

- A local government failing to maintain traffic signals

- Another driver dropping debris on the road

- The vehicle manufacturer producing a faulty car part

If your accident included a similar scenario, then you may be entitled to more damages than what first appeared. There is a statute of limitations concerning lawsuits that’s determined by the state the accident occurred in, so you should act fast to preserve your claim.

Labeling states as fault or no-fault is a bit misleading, and has understandably led to a lot of confusion regarding liability. So, who pays for car damage in a no-fault state? Generally, it’s the person or people responsible for causing the accident. The only damages no-fault settlement money applies to are those regarding bodily injuries.

This is exactly where Mighty can help: most people don't need a lawyer for basic no-fault or property-damage claims, but doing it alone often leads to mistakes that cost money. Mighty bridges that gap by helping you organize your documents, retrieve police reports and medical records, and understand the format insurers expect. It's everything people try to get from Google or DIY guides, but organized and supported through AI-powered technology.

FAQs About Who Pays for Car Damage in a No-fault State

Still confused about who pays in a no-fault accident? These common questions might help clear things up.

Still confused about who pays in a no-fault accident? These common questions might help clear things up.

Does Insurance Cover Things That Are Your Fault?

If you live in a tort state, your liability insurance will cover bodily injuries and property damage if the accident was your fault.

In no-fault states, each driver's personal injury protection insurance will cover their own injuries, regardless of who caused the accident.

If you're unsure which policies apply or how fault affects your claim, understanding these distinctions is important to avoid mistakes that insurers may use to deny or reduce your payout.

How Do Insurance Companies Determine Who Is at Fault?

Insurance companies apply the laws of the state in which the accident occurred to help determine who is at fault. They also review evidence surrounding the case to inform this decision, which is why it's important to get a police report and statements from witnesses.

Mighty can help you understand which evidence matters most, retrieve your police report, and assist with organizing witness statements and photos making it easier to have everything ready when insurers evaluate your claim.

Does the Police Report Automatically Go to Insurance?

A police report is not automatically sent to insurance companies after a car accident. Insurance companies will request a copy of the police report to help inform them of what occurred. They will then use that information while negotiating the no-fault car accident settlement to defend their offer.

Mighty can retrieve your police report and help you understand how to submit it to insurers in the format adjusters expect, helping ensure everything is filed properly and reducing the chance of delays or missing paperwork that could weaken your claim.

How Mighty Can Help with No-Fault Claims

Mighty can assist with several key aspects of no-fault claims:

● Document organization – Helping you organize and categorize your documentation (PIP vs. property damage vs. liability claims)

● Police report retrieval – Retrieving your police report and helping you understand what it contains

● Medical record retrieval – Obtaining medical records and bills from healthcare providers

● Expense tracking – Helping you organize and track medical bills, lost wages, and out-of-pocket expenses

● Understanding deadlines – Helping you understand important PIP deadlines (like the critical 30-day application window)

● Evidence organization – Assisting with organizing photos, witness statements, and repair estimates

● Understanding coverage – Helping you understand which state's no-fault rules apply and what different coverages mean

This approach means you get help organizing and retrieving the documents you need without attorney fees. For more complex claims or when litigation becomes necessary, you can transition to an attorney with everything already properly organized.

Mighty is not a law firm and does not provide legal representation. Mighty is an AI-powered platform that helps you organize documentation and retrieve important records for your insurance claim.

Unlike traditional law firms that charge 33%+ contingency fees, Mighty can help you organize your no-fault claim preparation from understanding PIP deadlines to organizing property damage documentation helping you keep more of your settlement while ensuring you're properly prepared.

Know Your Claim’s Worth—and Settle It

Serious injury or no injury at all, move your case forward instantly from your phone.

Thank you for submitting your information.

About the author

Maly is a seasoned professional with over 15 years of experience in the insurance sector, specializing in multi-line claims and customer service for personal injury cases. As the leader of Mighty’s Client Experience team, she leverages her extensive background to ensure clients involved in auto accidents receive the highest level of care and support. Maly’s expertise plays a crucial role in delivering exceptional service and fostering long-lasting client relationships.