Quick Answer

What Is Premises Liability?

Premises liability holds property owners responsible when their negligence leads to a visitor’s injury. It requires them to repair any hazards in a timely manner, or at least warn visitors of their existence in accordance with premises liability law. Failure to do so is grounds for an injured guest to recover damages through a premises liability claim.

When you’re a guest at someone’s house or place of business, there’s an expectation of safety that needs to be upheld. If you find yourself on the receiving end of an injury, it may be difficult to determine who is liable.

That’s where premises liability comes into play.

Premises liability is the legal concept that helps property owners, insurance companies and courts resolve disputes over responsibility when you’ve been injured on someone else’s property.

What Premises Liability Actually Means

Premises liability refers to the liability for failing to maintain the property in a safe manner. This obligation is also known as their duty of care.

A property owner violates this duty of care if their negligence leads to a visitor’s injury. It’s important to note that the status of the visitor is relevant in determining the property owner’s duty of care. As far as premises liability law is concerned, there are three types of visitors:

- Invitees: If you’re on a person’s property with their knowledge, with a mutually beneficial purpose, you’re considered an invitee. This applies to public buildings and businesses, like customers shopping in a store.

- Licensees: If you’re expressly invited onto a person’s property for reasons that fall outside of business intentions, then you are a licensee. This applies to people attending a friend’s cookout.

- Trespassers: If you're on someone’s property without their permission, you are considered a trespasser. This applies to a burglar stealing from a house.

Invitees are typically owed the highest degree of care, with the expectation that the property owner will mitigate all known risks and regularly inspect for hazards. Licensees are also owed a high degree of care, but since this type of visitor is usually reserved for residential properties, regular inspections are not expected.

Trespassers are still owed a low duty of care despite the property owner not consenting to their presence. The property owner still needs to warn trespassers of unexpected hazards.

Many people confuse premises liability with general liability, using the terms interchangeably. These are separate concepts, however, so it’s important to use them correctly.

General liability insurance may cover some premises liability violations, but it also covers injuries not resulting from negligence, like when a workplace is inherently dangerous and the business owner can’t reasonably eliminate all hazards.

The Most Common Premises Liability Claims

Premises liability is a broad term and covers many common occurrences like:

- Dog bites

- Slip and fall accidents

- Swimming pool injuries

- Business liability

- Negligent security

- Inadequate maintenance

- Roller coaster accidents

- Defective conditions

Even though these injuries have little in common with one another, they all hinge on the property owner’s failure to prevent the avoidable.

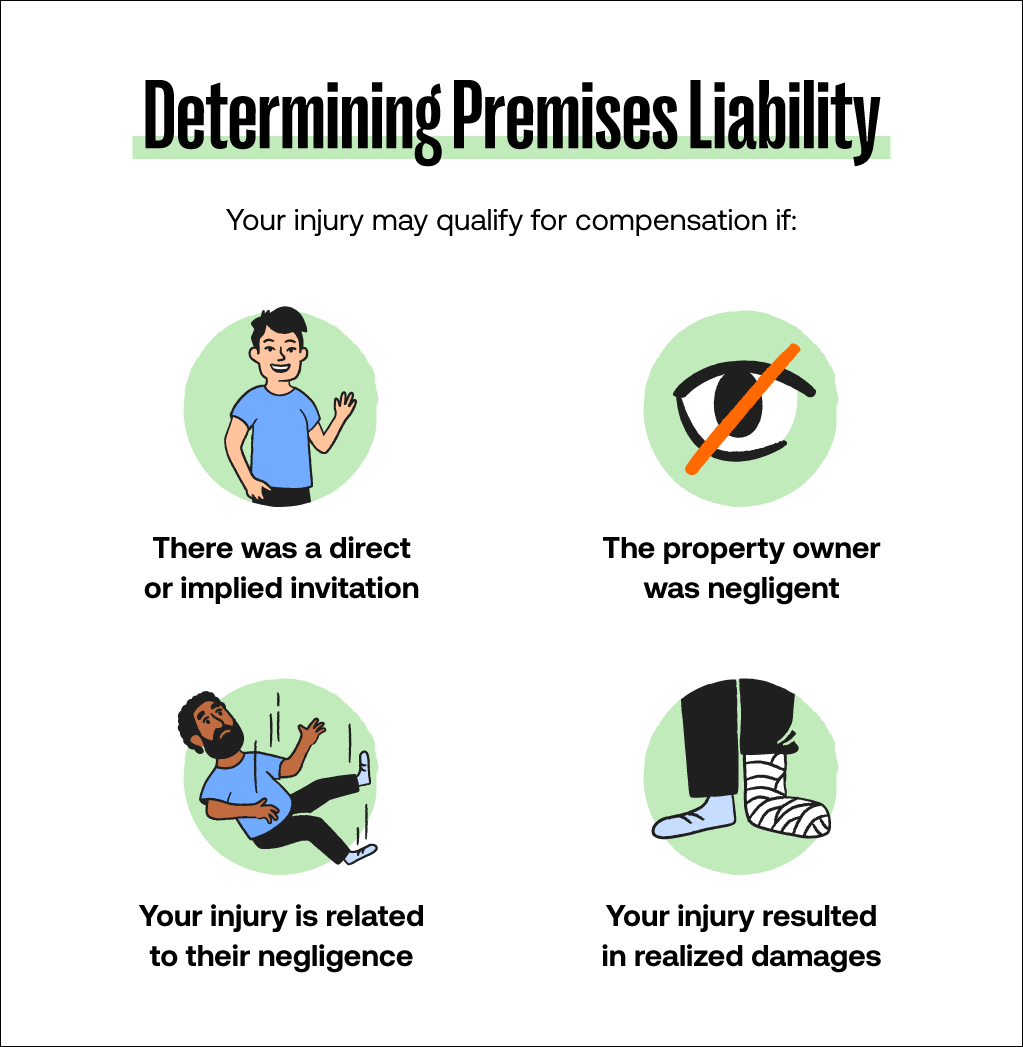

How To Determine Who Is Liable for Your Injury

For your injury to be eligible for a premises liability case, you’ll need to prove the property owner is at fault. To do this, you’ll need to meet certain premises liability case criteria:

- You were invited onto the property, either explicitly or implied. Some exceptions to this are premises liability injuries involving attractive nuisances, like swimming pools and trampolines. Attractive nuisances place a greater burden on the property owner to keep trespassers out.

- The property owner was negligent. If something was wrong with the property that the owner should have known about but failed to remedy, they acted negligently. If they had no time to act, such as a patron slipping within minutes of an unexpected storm, the store owner couldn’t have reasonably acted to prevent the injury. Animal bites are a different story, with regulations varying by state. In most cases, a dog owner would need to know the dog was dangerous before the incident for negligence to play a role.

- Their negligence led to your injury. In some cases, negligence may be apparent on the property, but if it had no involvement in your injury, then it’s irrelevant. For example, a loose handrail may need to be repaired but it can’t be cited as the cause of you slipping on wet grass.

- You can prove damages. If the incident resulted in no realized effects on your life, it will be difficult to receive compensation. Damages can involve the injury itself, medical bills as a result of treatment, or pain and suffering.

Exceptions abound with each of these criteria, so speaking with a qualified personal injury lawyer in your state can help make sense of the details surrounding your case.

Four Steps To Take if You’re Injured on Someone Else’s Property

Getting hurt on someone else’s property can be a scary situation, but it’s important to keep your composure to improve your premises liability claim.

- Take pictures/video: Immediately documenting the area can prove that the condition of the property led to your injury. Otherwise, the property owner can clean up the scene of the accident and make it your word against theirs. Look out for warning signs or the lack thereof that can prove negligence.

- Identify witnesses: Get the names and contact information of anyone who witnessed the accident. In the event of an investigation, you’ll want as many people as possible backing up your side of the story.

- Seek medical treatment: Receiving quick medical care can improve your healing process and let you know what to expect on the road ahead. Retain these medical records and bills to improve your chances of recovering damages.

- Don’t sign a release: The property owner or their insurance company may pressure you to sign a release of liability either immediately after the accident or in the days after. Speak with a lawyer before signing anything to ensure you don’t waive your rights to a fair settlement.

Following these four steps will make it very difficult for an insurance company to deny your claim.

Plus What Happens if You’re Partially at Fault

A property owner may try to deflect responsibility by claiming you’re partially at fault for your injury. In cases where this is true, most states have a system in place called comparative fault to help determine responsibility.

Visitors still have a responsibility to keep themselves safe, known as reasonable care. Comparative fault helps prevent visitors from acting negligently to place the entirety of the blame on the property owner.

It works by attributing a percentage of blame to both parties and uses that percentage to determine recoverable damages. There are three ways states choose to recognize partial fault:

- Pure contributory negligence: The injured party cannot collect damages if they are even 1% responsible for the accident.

- Pure comparative fault: The injured party can collect damages even if they are 99% responsible for the accident, but they can only recover the percentage that they are not at fault. So, if you’re found to be 90% responsible for a $20,000 injury, you can only recover $2,000.

- Modified comparative fault: This is applied in two ways depending on the state. The 50% rule means the injured party cannot recover damages if they are responsible for 50% of the accident. The other application, the 51% rule, means the injured party cannot recover damages if they are 51%at fault.

The level of responsibility is generally determined by the judge or jury assigned to the case.

And What To Expect From Homeowners Insurance

If you’ve been injured on someone else’s property, you’ll likely be dealing with their homeowners insurance first to receive compensation. Their insurance will look for any reason to deny your claim, and that usually involves pointing the finger at you.

The insurance company may deny your claim entirely if your injury was the result of an intentional act on your part or the part of the property owner. For instance, if the property owner attacked you then you’ll likely need to pursue action against the property owner personally. The same applies to any reputational damage you may feel the property owner is responsible for.

Premises liability can be a complicated business, but learning your state’s laws and how to react after being injured on someone else’s property can improve your chances of winning a claim.

Of course, speaking with a qualified personal injury lawyer is recommended to make the personal injury settlement process as easy on you as possible.

FAQs for When You’re Injured on Someone Else’s Property

Here are some answers to questions people commonly have regarding premises liability and personal injuries.

What Damages Can You Recover From Your Injury?

If a person is injured on someone else’s property, they may be able to recover damages regarding their:

- Medical expenses

- Pain and suffering

- Lost wages

In rare cases, the injured party may recover punitive damages if the property owner acted recklessly or intentionally harmed them.

If the accident resulted in the wrongful death of a person, their family may be able to recover damages on behalf of the decedent.

What Dangerous Conditions Does the Property Owner Have to Warn About or Fix?

Property owners have a duty of care to fix all known dangerous conditions on their property, like loose handrails or icy steps. If it’s impossible to fix a hazard as soon as it is known, they are required to warn visitors and do their best to reduce the risk of harm until it can be repaired.

Who is Responsible For Injuries on Public Property or in Government Buildings?

If a personal injury occurs on government-owned property, the government agency in charge of the property may be held responsible, only if the injury occurred as a result of negligence by the agency.

Know Your Claim’s Worth—and Settle It

Serious injury or no injury at all, move your case forward instantly from your phone.

Thank you for submitting your information.

About the author

Luke is a warm-hearted and highly skilled legal operations expert with an impressive 8-year track record in the personal injury field. As the Client Operations Lead at Mighty, he is dedicated to providing exceptional support, transparent communication, and genuine empathy to clients during their challenging journey. His expertise in streamlining processes and implementing cutting-edge technology makes him an indispensable ally for clients, case managers, and attorneys in their pursuit of justice.